The last week (December 10th — December 17th, 2017), Jeff Kinney requested my answer at Quora about this interesting question:

Which Crypto currency is the best to invest now $2500 (long-term investment)?

Then, Jeff Kinney sent me a different question about Ripple (XRP):

Is Ripple a good investment? How I do buy Ripple?

This was my answer:

But, as a personal finance geek who loves numbers and facts so much, I felt that there was an opportunity to bring more light to my answers about Ripple (the company) and $XRP (the digital asset).

What is Ripple?

The first time I heard about Ripple was in 2016 when I found a very interesting whitepaper written for the specialists of the company called “A Protocol For Interledger Payments”, which explains in great detail how this protocol works, the technical background behind it and why it’s relevant today a solution like that.

So, what is Ripple (the company)?

I will use its own words here:

Ripple provides global financial settlement solutions to ultimately enable the world to exchange value like it already exchanges information — giving rise to an Internet of Value (IoV). Ripple solutions lower the total cost of settlement by enabling banks to transact directly, without correspondent banks, and with real-time certainty of settlement. Banks around the world are partnering with Ripple to improve their cross-border payment offerings, and to join the growing, global network of financial institutions and market makers laying the foundation for the Internet of Value.Ripple is a venture-backed startup with offices in San Francisco, New York and Sydney. As an industry advocate for the Internet of Value, Ripple sits on the Federal Reserve’s Faster Payments Task Force Steering Committee and co-chairs the W3C’s Web Payments Working Group.

As a fan of simplicity, I knew that there had to be a simpler answer to the question about what is Ripple and what it does? And I found it in a live interview made by Martin Arnold (The Financial Times) to Daniel Aranda, Managing Director For Europe at Ripple:

In the interview, Daniel said:

Ripple is a cross-border payments network, and the members of the network are financial institutions. We work with banks as well as non-bank financial institutions, and they use Ripple as a way to move funds around the world to other financial institutions. And where the blockchain portion comes in is in really helping to coordinate things like settlement, so when a debit occurs to the account of the sender, is coordinated and synchronized with the credit accuracy account of the receiver.And we are also deploying digital assets cryptocurrencies, tokens of equity management as well. So, we are really trying to build a next generation network in terms of people how can move funds around to service new kinds of demands we are seeing on the market.

I encourage you to watch the entire discussion. Believe me, it worth of your time.

Then, I began to search more information about the protocol and the company behind it: Ripple. In the middle of my search, I found another interesting whitepaper called “The Cost-Cutting Case for Banks: The ROI of Using Ripple and XRP for Global Interbank Settlements”, and I realized that this could be huge in the next 5 to 10 years.

Inside the whitepaper, I found two particular parts which made me to jump of my chair:

This model includes a conservative assumption of hedging costs with initially high volatility of XRP. However, institutional holdings and active trading of XRP can greatly reduce the volatility of XRP, significantly lowering the hedging costs. In a low volatility state, assuming the volatility of XRP is the same as that of a basket of liquid global currencies, costs can decrease an additional 3.8 bps ($10 billion system-wide) or 60 percent compared to the current system, translating to

total system-wide cost savings of over $33 billion annually with lower volatility of XRP.

Specifically, Ripple can eliminate 6.8 bps or $18 billion annually in liquidity and payment operations costs. Implementing Ripple with XRP, which further improves liquidity and treasury operations costs, can lead to a total savings of 8.8 bps or $23 billion annually. As the volatility of XRP approaches that of a global currency basket, cost savings can amount to 12.6 bps or $33 billion annually.Furthermore, as banks globally adopt Ripple and as liquidity costs

are eliminated, there is a real possibility that the marginal cost of international transactions approaches zero. To accelerate market thickness and reduce volatility for XRP, Ripple will soon introduce an XRP incentive program to algorithmically rebate market makers who provide liquidity through XRP.

Let me repeat the number: a cost reduction to almost 60% compared with the current system (SWIFT I suppose), for a total annual saving of $33 Billion globally.

When I read those numbers, I immediately gathered the opportunity behind Ripple and its Internet of Value vision.

That’s why in my answers at Quora, I made a clear point: XRP is not in a bubble like Bitcoin; it has a real multi-billion industry behind and Ripple is working with more than 100 financial and non-financial organizations at global scale to get on board on their RippleNet.

Here are some of the most prominent banks and financial organizations working with Ripple:

- American Express (NYSE: AXP)

- Canadian Imperial Bank of Commerce (NYSE: CM)

- Banco Santander (NYSE: SAN)

- Swiss-based UBS (NYSE: UBS)

- Japan Bank Consortium (JBC), a collection of 61 Japan-based members

- RAKBANK (United Arab Emirates)

- Standard Chartered Bank (Singapore)

- Axis Bank (India)

- Barclays (United Kingdom)

When Ripple announced they were working with Axis Bank, Standard Chartered and RAKBANK, I quickly began to search more about the opportunity.

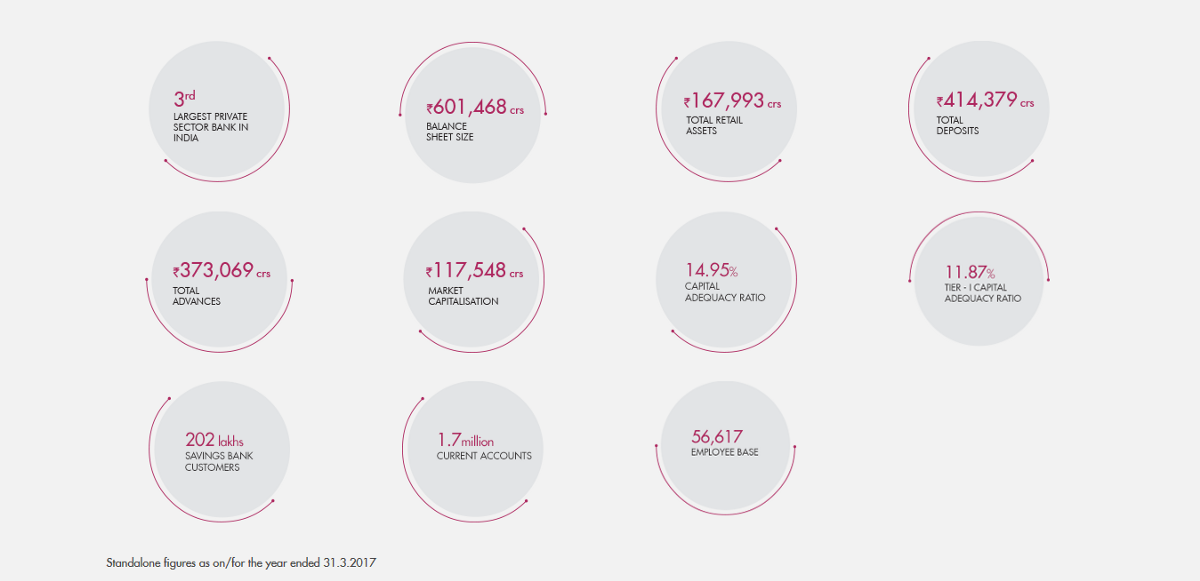

First case: Axis Bank

Using their own words in the last financial reports, you can see the impact that could create Axis Bank inside RippleNet:

Incorporated in 1994, Axis Bank has emerged as one of India’s most trusted banks and the third largest in the private sector. It is among the country’s first new generation private sector banks, and offers the entire spectrum of financial services to customer segments, spanning large and mid-corporates, SME and retail businesses.Over the years, the Bank has developed long-term relationships with its customers by being their preferred financial solutions partner, leveraging deep insights and superior services.

Axis Bank has also taken significant steps to simplify banking for its customers by the smart use of technology. The Bank has always focused on meeting the financial needs of its customers by providing high-quality products and services through regular customer engagements.

Second case: Standard Chartered

Ummm, well done SC:

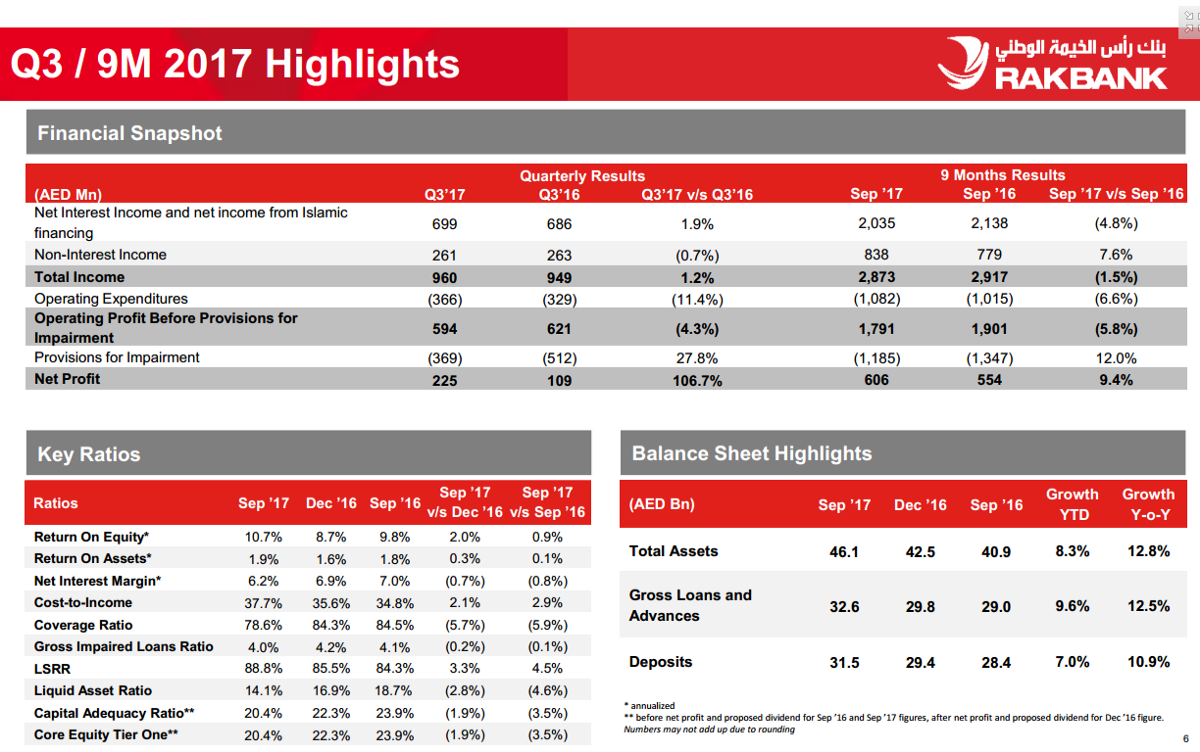

Third case: RAKBANK

Analyzing the last financial report of Q3 of 2017, you can see the big numbers behind RANKBANK

It’s great to see this kind of organizations working with Ripple, and based on the information shared in the article about the announcement; this could be a terrific opportunity:

For Standard Chartered and Axis Bank, the Ripple-powered corporate payment service will allow each bank to offer their business customers an enhanced payments experience, ultimately enabling their end-customers to manage their cash flow, costs, and float better.By our estimates, there are between 200–300 large, international corporates with regional treasury hubs in Singapore. These corporates span industries including fast-moving consumer goods (FMCG) and retail.

Often these corporates manufacture their products in India before shipping them to Singapore for worldwide distribution. In fact, the Singapore-India trade corridor is worth $15 billion.

Ripple-enabled cross-border payments will help unlock this corridor on both sides for Standard Chartered and Axis Bank.

It’s also never been more important for retail remittances to be instant, efficient, and secure between the UAE and India. Retail remittances between the two countries are significant and growing, thanks to the large Indian workforce in the UAE.These workers send a significant proportion of their salaries home every year — nearly $12.6 billion annually — which RAKBANK wants to support with faster, easier, and more transparent payments.

Individual retail remittance payments are usually lower in value, but higher in volume. Processing these over RippleNet will allow RAKBANK to offer their retail customers an easier, more affordable experience, helping them to increase their market share in this crowded and competitive space.

So, this is part of the network effect Ripple is causing in the banking world. Precisely focused on the network effect and many other things, Brad Garlinghouse (CEO at Ripple) gave a very interesting Q&A session on Wednesday December 20th, 2017:

And on Thursday December 21, 2017, was the Q&A with David Schwartz (aka JoelKatz), the Chief Cryptographer at Ripple:

If you want to invest on XRP, you must watch these talks.

XRP as a long-term investment

Now, let’s analyze the long-term investing opportunity behind the digital asset of Ripple: $XRP. According to CoinMarketcap, XRP has a market capitalization right now of $40 Billion, and its price at this moment is $1.03 USD (December 22th, 2017):

Why XRP is superior to other cryptocurrencies?

Ripple’s team answered these questions in Tweets:

Now, analyzing the market opportunity behind Ripple, I found this quote which is perfect for this:

What is the Internet of Value?Our vision is for value to be exchanged as quickly as information. Although information moves around the world instantly, a single payment from one country to another is slow, expensive and unreliable. In the US, a typical international payment takes 3–5 days to settle, has an error rate of at least 5% and an average cost of $42. Worldwide, there are $180 trillion worth of cross-border payments made every year, with a combined cost of more than $1.7 trillion a year.

That´s why Ripple (the company) is working in several solutions not just only for banks, but for corporations too; to help them to alleviate these massive costs in annual transactions. These solutions are:

- xCurrent: It is Ripple’s enterprise software solution that enables banks to instantly settle cross-border payments with end-to-end tracking. Using xCurrent, banks message each other in real-time to confirm payment details prior to initiating the transaction and to confirm delivery once it settles. It includes a Rulebook developed in partnership with the RippleNet Advisory Board that ensures operational consistency and legal clarity for every transaction.

- xRapid: It is for payment providers and other financial institutions who want to minimize liquidity costs while improving their customer experience. Because payments into emerging markets often require pre-funded local currency accounts around the world, liquidity costs are high. xRapid dramatically lowers the capital requirements for liquidity

- xVia: It is for corporates, payment providers and banks who want to send payments across various networks using a standard interface. xVia’s simple API requires no software installation and enables users to seamlessly send payments globally with transparency into the payment status and with rich information, like invoices, attached

For myself, the most interesting of these products is xVia. Why? Because it could be even a larger market.

Just consider these numbers of 3 major corporations, which could decide to work with Ripple:

- Alibaba Group (BABA): the company works with 75% of consumer brands in Forbes Top 100 Most Valuable brands on Tmall

- Shopify (SHOP): announced that collectively retail shops sold over $1 Billion in GMV on November 28th, 2017, and the company is powering 500,000 businesses globally

- Apple (AAPL): works with many suppliers overseas

Could you imagine if these companies worked with Ripple in the future? Not only public companies, but private corporates as well. Ripple´s secret weapon here? The incredible list of institutional investors behind the company:

You should wondering: Why all this matter? Because XRP will be the digital asset in these transactions, and it could grow its value in the long term.

That´s why we at Capital Latino bought a significant chunk of XRP for our investment portfolio, thinking always in the long term.

Our advice? Act today and add somes XRPs to your portfolio as well. We made the same recommendation to some of our clients in our Facebook group.